|

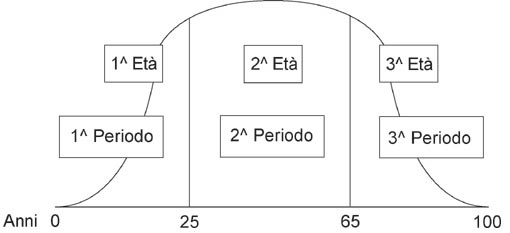

1st PERIOD (1ST AGE)

This is the period which goes from birth to the beginning of working age and it is secured by family.

2nd PERIOD (2nd AGE)

It is the working period in which men are able to earn their livings by their own forces.

They try at the same time to save part of their earnings to face out old age with serenity.

(art.38 Constitution)

3rd PERIOD (3rd AGE)

It's the hardest period because, unfortunately, men can't often count on their own forces.

Therefore our life can be resumed by this simple graph:

Even the 38th article of our Constitution acknowledges the third period as the most critical for our maintenance:

" Workers are entitled to be provided with all means old age requires".

" State's organs and institutions fill the duties provided for by this article"

This is a clear concept that may not cause a misunderstanding: the State takes care and provides men with adequate means for their old age

But Governments, though they respected the constitutional principle, applied together with the laws a method of calculation that has no relation with the principle of the article 38.

No mind of good sense and normal capacities would conceive this method of calculation if not as an easy and immediate mean to take away that legitimate "richness" that Constitution provided for any person able to get a living.

That is to say with the forced saving of a part of the labour cost that however the employer has and charges on the selling price of his products: on average it affects by 43 %

Though adequate means are provided, their application is absolutely incorrect, either in terms of social consideration or in concrete results, distorting constitutional principles, particularly the articles 38 and 47 of Constitution

The evaluations characterising the calculation of the pensions are in short:

A) Working people must pay for retired people.

Reflection: if anyone doesn't work anymore the retired person must die.

B) The allocation of the pension is calculated for 20 years of life only.

Reflection: since we retire, we have only 20 years before dying.

The technical rate of revaluation is approximately 1,7 % on an amount which is lower than the amount paid.

.

Reflection: who benefits of the difference between 4% and 1,7%?

What is the clear and simple request which is to be realized?

Paid-up contributions have to be capitalized and returned to the rightful owner when he retires on a pension.

.

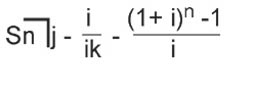

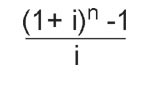

The financial formula for the calculation of capitalization

is expressed like that:

= accumulated capital when one retires

= coefficient of contributions because they're paid monthly (it varies according to the varying of the rate)

= contributions paid every year and capitalized with compound interest

The model in figures is the following:

A) Since contributions in one year and for all 35 years of work are always 8.493,13 only and the rate is always by 4%, we multiply 8.493,13 by 76,5983

(coefficient of capitalization composed of monthly payments deferred of one euro)

B) we multiply then this product corresponding to the monthly payments, that is 1,01820351

C)So, after 35 years, considering the contributions and the rate listed above, we have:

662402,19

D)This is nothing but the Capital of our sole ownership at the end of the work relation

E) Capital which invested at 4% will annually give an interest, or the annual pension of 26.469,09= 2208,01 per month

Traduzione a cura di Pietro Frassica

e-mail : pierfras@tiscalinet.it

|